The Annual IMF meeting held this month at Washington deliberated on global and regional economic outlook. In this regard we would like to hear from you on this.

- What is your outlook on Global Economy?

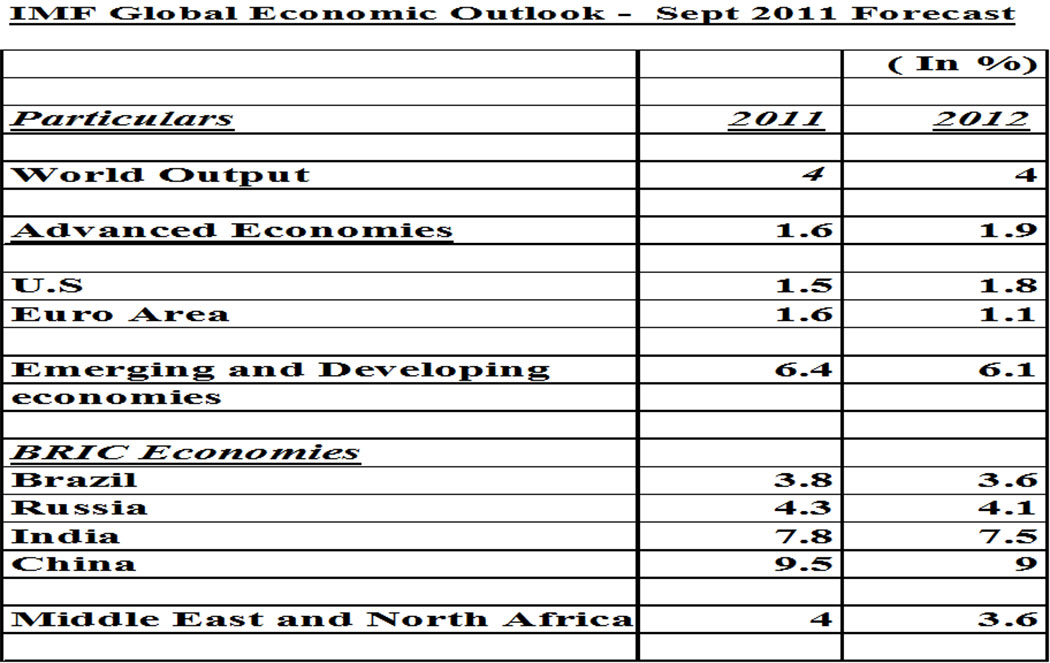

- Global growth will moderate to about 4 percent through 2011 and 2012 , from over 5 percent in 2010.

- Real GDP in the advanced economies is projected to expand at an anemic pace of about 1.6 percent in 2011 and 1.9 percent in 2012.

- Global activity has weakened and become more uneven, confidence has fallen sharply recently, and downside risks are growing.

- Advanced economies growth for 2011 revised from 2.2% in June 2011 to 1.6% currently.

Major advanced countries on which growth has been lowered

- US economy growth for 2011 revised from 2.5% growth in June 2011 to 1.5% currently. The downgrade and fiscal issues have impact on medium term growth.

- Euro Area growth for 2011 revised from 2.% growth in June 2011 to 1.6% currently due to slower growth in Germany, France and Italy.

- Germany, France and Italy growth for 2011 have been revised from 3.2%, 2.1%,1% respectively in June 2011 to 2.7%, 1.7% and 0.6% currently. The Euro crisis is impacting growth in these countries.

- Emerging and developing economies growth for 2011 revised from 6.6% in June 2011 to 6.4% currently.

- Middle east and North Africa outlook for 2011 revised down to 4 % from 4.2% in June 2011.

- We are seeing a situation of risks challenging the current global growth in the medium term.

- It is a situation of rising risks and slowing growth.

- What are the major reasons for this slowing growth?

- Fiscal consolidation in advanced economies can slowdown growth.

- In the United States, the handover from public to private demand is taking more time than anticipated.

- In addition, sovereign debt and banking sector problems in the euro area appear much more deeper than expected.

- In emerging and developing economies, capacity constraints, policy tightening, and slowing foreign demand are expected to dampen growth to varying extents across countries.

- The disruptions resulting from the Great East Japan earthquake could have had some impact on the output of automobile sector (particularly cars.) in advanced economies due to supply chain disruptions.

- The sudden spike in oil prices in 2nd quarter of 2011 may have mildly impacted the global economic outlook.

GROWTH COULD BE SUPPORTED BY

- The rebound of activity in Japan –Industrial production is now growing rapidly, business sentiment is improving sharply, and household spending is recovering quickly.

- Proper Monetary policy and Prudent fiscal discipline.

- What are the key challenges to global economy?

- Insufficiently strong policies to address the legacy of the crisis in the major advanced economies.

- Increase in financial volatility- Bonds, Commodities equities volatile in the last 2 months.

- Strain noted in inter banks- Inter-bank markets are again under strain, and some banks reportedly are finding it difficult to continue to obtain funding.

- Inflation in emerging economies.

- Bring down Unemployment.

- House prices show no signs of stabilizing in key crisis-hit economies such as the United States and Spain.

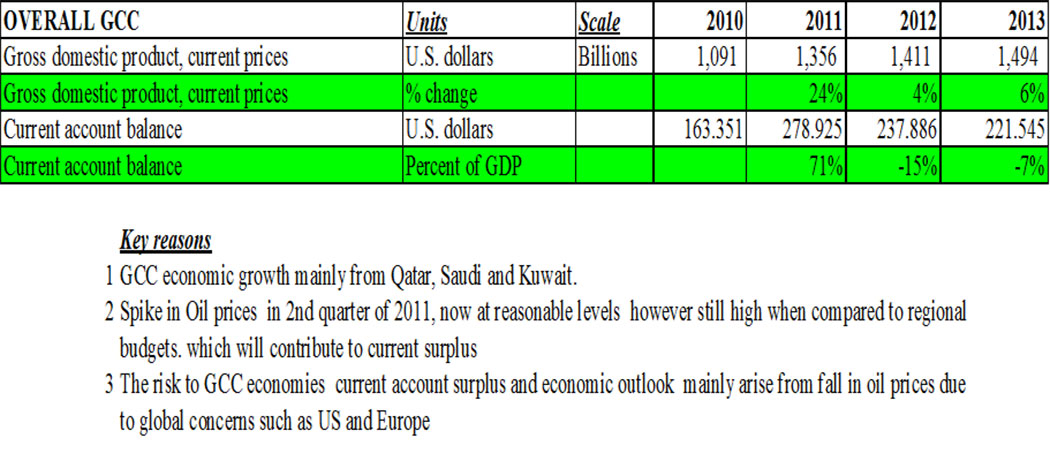

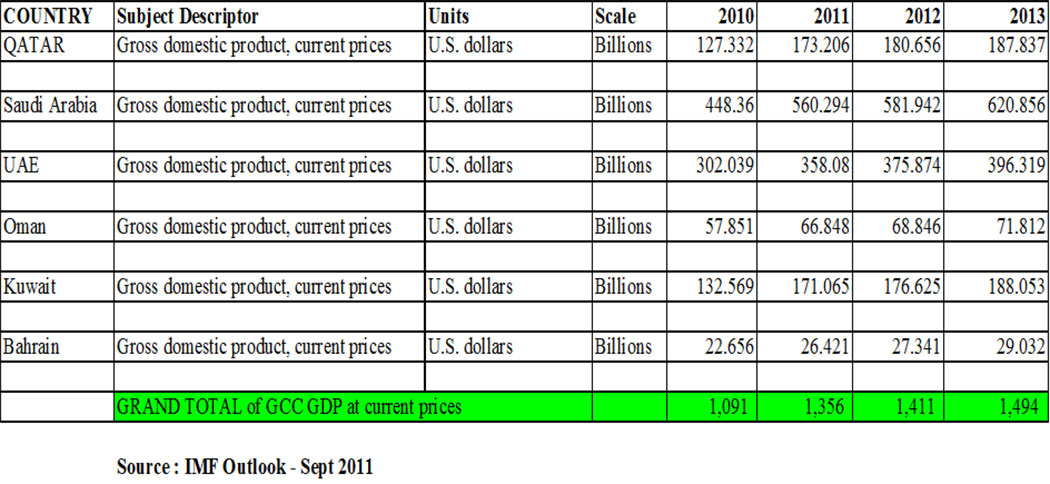

- What is your overall outlook in GCC economy?

GDP at current prices (As per IMF)

GDP at current prices (As per IMF)

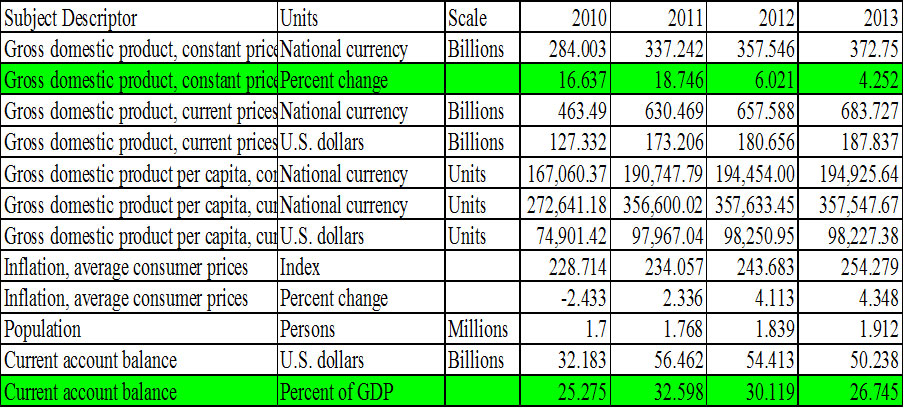

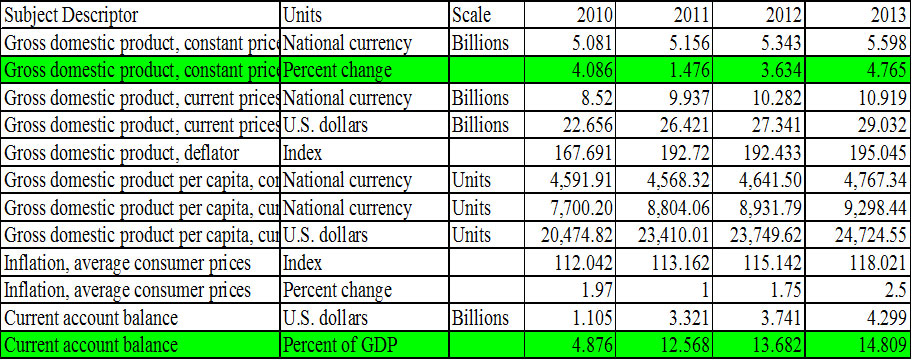

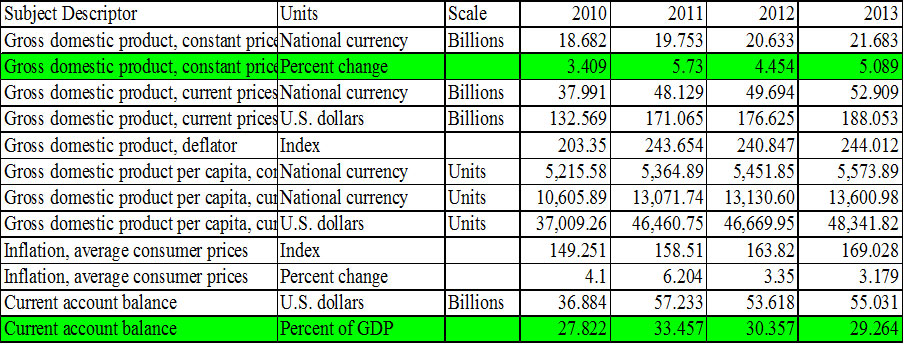

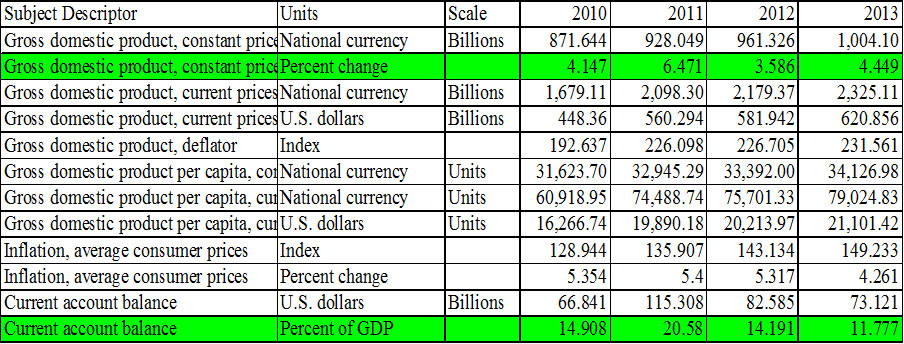

- What is your outlook on Kuwait and Saudi economy?

- Kuwait has been revised outlook on upward side to 5.7% for 2011( Earlier it was expected 5.3% in June 2011 ).

- Kuwait’s budget surplus stood at $15.3 billion in the first two months of its 2011/12 fiscal year, larger than a year ago on higher-than-projected oil revenue and lower spending.

- Kuwait’s inflation had eased to an 11-month low of 4.6% in July 2011.

- Saudi Arabia, with the world’s biggest petroleum reserves, will see GDP grow by 6.5 percent in 2011 which is down from 7.5 percent in IMF’s previously forecast in April 2011.

- Saudi’s inflation had slowed to 4.8% ( Yoy) in August 2011 from 4.9% in July 2011 as rise in transport and housing subsided.

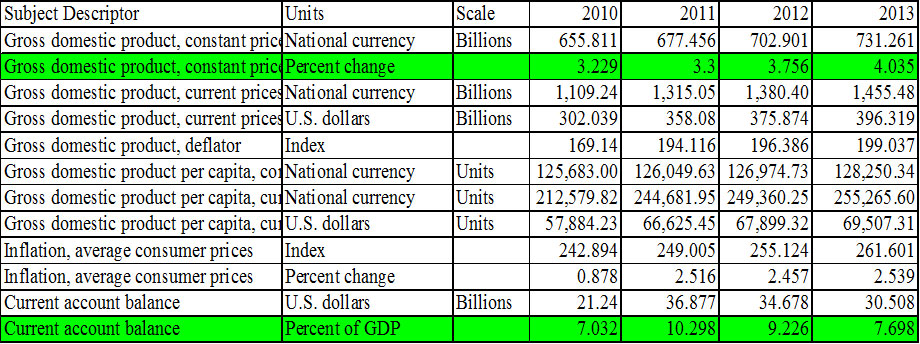

Kuwait Economy (As per IMF – Sept 2011)

Saudi Arabia Economy (As per IMF – Sept 2011)

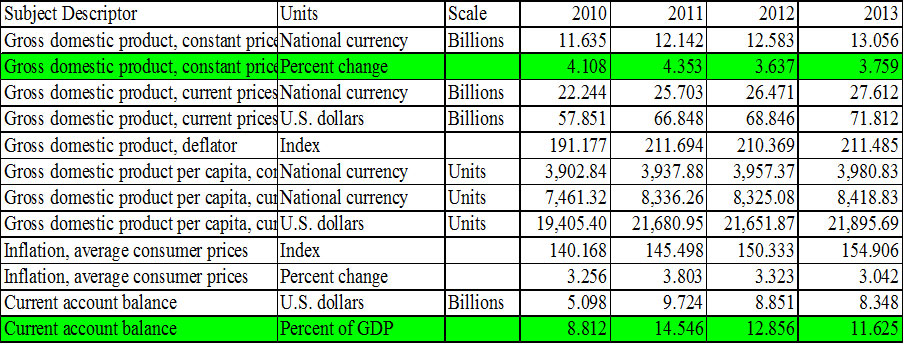

- What is your outlook on Oman, Bahrain and UAE ?

- Oman ‘s growth is expected to be 4.4% in 2011.

- Oman’s inflation is expected to be around 4- 4.5% in 2011.

- Bahrain’s growth is expected to be around 1.5% in 2011 instead of 3.08% due to regional tensions. Inflation is also expected to fall.

- UAE expected 3.3% growth.

- UAE ‘s inflation slowed to 0.6 per cent in August 2011 from 1.3 per cent in July 2011.

Bahrain Economy (As per IMF – Sept 2011)

Oman Economy (As per IMF – Sept 2011)

UAE Economy (As per IMF- Sept 2011)

- How has Qatar economy performed in recent times?

- This year expected to grow at 19%.

- The quarterly GDP at current prices is estimated at 141.84 billion Qatari Riyal in the Q1 of 2011. Compared to the estimates of Q1 of 2010 with 110.46 billion Qatari Riyal, this represents an increase of 28.4%.

In 1st quarter 2011 Gross value added ( GVA)

- In Mining and quarrying rose by 44% since 1st quarter 2010.

- In Manufacturing sector rose by 20% since 1st quarter 2010.

- Transport and communication rose by 20% since 1st quarter 2010.

- Finance, Insurance and real estate rose by 10% since 1st quarter 2010.

- Government services rose by 20% since 1st quarter 2010.

Note : Gross value added + Taxes – Subsidies= GDP

Qatar Economy (As per IMF- Sept 2011)